Soaring inflation and Real Assets – a match made in heaven?

We would need to delve back into past times to understand what life with high inflation looks like, because let’s face it, a bulk of the UK working population haven’t ever witnessed such a time. Of course, there are still plenty who can recall the 1970’s inflation boom and the measures taken by a Margaret Thatcher led government to address the issue.

But first, let’s recap on what inflation actually is. Referred to by many as the ‘cost of living’, inflation is the term used to describe the increase in prices over time. Inflation is calculated by adding up the average prices of thousands of different things and comparing them to the prices of the same goods a month ago. This means there is a list somewhere of the specific things that count towards inflation in any given country, and each month someone has to go out and check the average prices of all these things.

How quickly those prices go up is called the rate of inflation. Inflation is shown as a percentage, and tracked via the Consumer Price Index (CPI). In short, if a pint of milk costs £1 and rises by 5p, then milk inflation is 5%. This, along with any prices changes in other tracked goods (up or down in price), is then crunched together to provide a percentage of the average rate of change in prices of consumer goods. This can result in a rise (inflation) or decline (deflation) in the cost of living.

With inflation rising across multiple goods and services at any one time, typically due to gaps in the supply and demand chain, the impact can be somewhat damaging to people’s cost of living, especially if interest rates and wages do not keep pace.

On the 16th of March, the Federal Reserve approved the first interest rate hike in the US in over three years, bringing the US interest rate to 0.5%. With a further six rate rises expected over the remaining Federal Reserve meetings this year, rates in the US, according to analysts could reach 1.9% before the end of 2022.

On Thursday the 17th of March the Bank of England followed suit and lifted UK interest rates to 0.75% in their third consecutive interest rate rise since the December 2021 lows of 0.1%

These increases to interest rates in both the US and UK have been in response to rising inflation, which is now expected to be at 8.5% in the US by the end of Q1, and expected to reach 8% here in the UK later this year.

Inflation has been a concern of Central Banks for quite some time now since they originally slashed interest rates at the onset of the pandemic to combat the lockdowns which initially crippled the economy. However, there has now been several factors, including supply chain issues, labour shortages, rising energy prices, and more recently, the Russian invasion of Ukraine that has accentuated the issue and forced the Central Banks’ hands into introducing rate hikes.

Although it has been decades in the UK since we have experienced inflation to the heights we are currently seeing – in the 1970’s inflation reached over 25%, inflation in the UK is currently at 5.5% (March 2022). This issue cannot be ignored, and quite rightly the Central Banks will endeavour to reduce the impact inflation has on people.

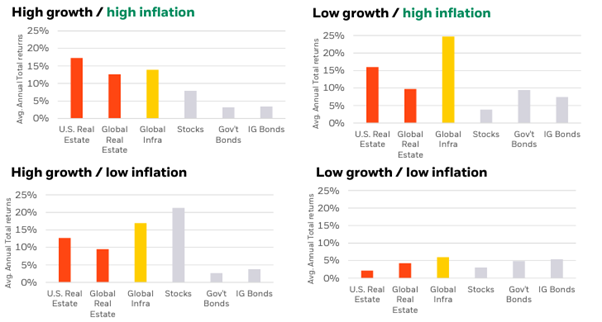

However, if we look back to when the Consumer Price Index has been at 2.5% and above, real assets, which includes real estate, infrastructure, and commodities, have outperformed other asset classes such as equities and bonds.

This is due to rental leases, revenue streams, and material costs each having either direct or indirect links to inflation and therefore the ability to capture inflation through greater income growth. Real estate rental leases are commonly linked to inflation, occasionally with expense pass throughs written into their contracts, which allows the asset to appreciate in line with inflation without being negatively affected by rising costs.

In similar vein, many infrastructure assets, including most of the power and utility investments, have a direct link to inflation through their regulations and long-term revenue contracts, providing them with inflation protection. With the war in Ukraine unfolding over the past few weeks, it has been evident that supply and demand disruptions have caused a sharp increase in both inflation and commodity prices.

In addition to this, companies from sectors with revenue streams linked to the above assets can be expected to perform well in the current economic environment. The large capitalisation dominated index that is the FTSE100 has fared far better year-to-date than some of its developed world counterparts such as the S&P500, providing returns of 2.22% as of 22nd March 2022. This is primarily due to the index having high weightings in sectors such as Financials, Industrials, Materials, and Energy, each of which tend to outperform in high inflationary periods. Due to this, the UK large capitalisation equity space is also an area of interest

For the past 12-18 months at Fiducia we have been of the opinion that inflation would not be transitory, and that Central Banks were behind the curve on interest rate hikes. Despite their recent rate hikes, we believe this to now be a reactive measure rather than a pre-emptive one, and inflation will now be far stickier than markets had once priced in. The recent invasion of Ukraine has caused unforeseen circumstances, which has also led to our expectations for economic growth in both 2022 and moving into 2023 to be considerably lower.

Due to the deterioration in the growth and inflation outlook, the valuation of equity markets and therefore the total return we expect from the various market indices has lowered. However, in anticipation of a high inflation environment, which we expected, for the past year we have been periodically increasing our exposure to real estate and infrastructure, through funds such as Urban Logistics, Foresight Sustainable Real Estate, and Foresight Global Real Infrastructure, adding to our commodity exposure through Wisdomtree Industrial Metals, and Wisdomtree Physical Gold, which provides a direct inflation hedge, and finally increasing exposure to these asset classes indirectly through UK large capitalisation companies via the iShares 100 UK Equity Index.

The Fiducia Wealth Management Core range of portfolios real assets allocation is now at a weighting of 20-25% of the portfolio, with scope to increase this further to 40-50%. With the capability to allocate capital to real assets, and as demonstrated by the figures created by Blackrock Asset Management, and the reasons outlined above, we are confident our portfolios will perform well in the high inflation/low growth environment we find ourselves in.

So, to summarise and answer the original question ‘Soaring inflation and Real Assets – a match made in heaven?’ history shows us that during these unorthodox times of high inflation and low growth, an investment portfolio weighted towards real assets can and will outperform equities and bonds. This can be seen in the charts below.

Keeping pace with inflation can be difficult and ensuring your money tomorrow is still as valuable, if not more valuable than it is today, requires strategic asset allocation.

If you’d like to speak to our team of award winning Chartered Financial Adviser about your existing portfolio, please do not hesitate to contact us on 01206 321045 or email email@fiduciawealth.co.uk

{kind=link}