While BRIC will undoubtedly remain a source of rich returns for some time to come, the emerging markets umbrella casts a far wider shadow than just BRIC, encompassing a vast array of alternative, less mainstream economies that have the potential to follow the high growth path previously trodden by BRIC. A subset of such economies is frontier markets, a group which plays host to such nations as Nigeria, Kazakhstan and Vietnam. While accepting they are somewhat of a niche play, we have actively incorporated a small frontier market allocation within our higher risk mandates since late 2009 as, in our view, the benefits they bring to an overall portfolio alongside their long term prospects make for a strong investment case.

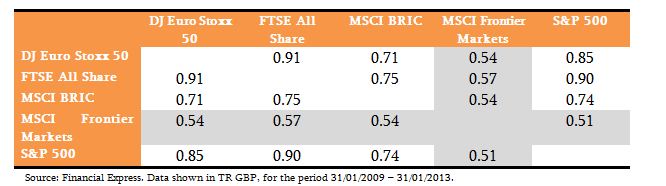

From the perspective of portfolio theory, a key pillar of the case for frontier markets is the diversification benefits that they provide within an overall portfolio context. When one scrutinises the correlation coefficient[1] of the frontier markets index relative to an assortment of global equity indices, an encouraging picture emerges, as portrayed in the following table:

At least over the past four years, frontier markets have enjoyed low correlation to a number of equity indices the world over, which is a highly prized and much cherished characteristic to possess in a world where global stock indices tend to look to one another for direction. These correlations take on added significance when viewed through a portfolio-wide lens, as they mean a frontier markets fund which is seemingly highly volatile in isolation can actually reduce overall portfolio volatility, as its inclusion would broaden the source of returns and reduce the extent to which the equity component behaves in a similar fashion.

Turning to the underlying economics of frontier markets, at a macro level the picture is a favourable one. GDP growth has consistently been at high single-digit, if not low double-digit, levels since 2001, far outstripping Western markets, with this trend forecast to continue. The indebtedness of economic agents, from consumers to governments, is healthy, thereby improving disposable incomes, sustaining domestic demand and avoiding the crippling effects of deleveraging[1] which currently blight the developed world outlook, while a strong balance of payments position ensures frontier markets are not too dependent on others. Demographics are another feather in the frontier markets’ cap, with data[2] showing that out of a total frontier market population of 842 million, approximately 60% are below the age of 30, ensuring a strong labour force is in place to underpin economic growth for years to come. At a micro level, constituents of the frontier markets cohort have now deposed China as the world’s cheapest labour market. In Bangladesh, for example, labour costs per hour are approximately one-tenth of those in China[3], a statistic which will no doubt entice companies the world over to re-locate production efforts, having positive ramifications for the local economy. Furthermore, frontier market companies tend to be the subject of less analytical research, meaning there are real opportunities to exploit mispricing occurrences and realise large returns over the long term.

In making the case for frontier markets, it would be remiss to neglect the risks that accompany such an investment. Liquidity can be a cause for concern, as equity indices in the space tend to be less developed than, and less integrated with, the traditional equity indices such as those in the UK, US and Europe. Political instability and corporate governance problems are additional factors that need to be evaluated, but as frontier markets expand their presence globally and hence assimilate with the developed world to a greater degree, one would expect these fears to lessen. Currency fluctuations are another factor, as is the susceptibility of frontier markets to high levels of volatility as their cyclical nature exposes them to swings in investor sentiment. Despite these risks, however, we feel they can be navigated effectively to secure strong returns, and are adequately compensated for by the compelling long term investment case. Including frontier markets in a higher risk portfolio is, therefore, a rewarding exercise in our view.

[1] The BRIC nations comprise of Brazil, Russia, India, and China.

[2] The correlation coefficient indicates the extent to which two variables co-move, using a scale of -1 to +1. A figure of +1 would mean the two are perfectly positively correlated, moving in tandem, whereas a figure of -1 would mean the two are perfectly negatively correlated, which is the opposite.

[3] Deleveraging is the process of debt reduction.

[4] Source: Schroders.

[5] Source: Schroders.