Can I Retire with £350,000 in investments and pensions? How Cashflow Planning Can Help

Posted in Pensions & Retirement on 14.07.26

Can I Retire with £350,000 in investments and pensions? How Cashflow Planning Can Help

One of the most common questions we hear is, “Do I have enough to retire?” Sadly, there is not a singular figure that works for everyone. Each person’s preferences for retirement are different, some want to travel whilst they can, others are happy working on their garden, some want to retire as soon as possible, others can see themselves working many more years.

The amount you’ll need in retirement depends on your lifestyle, when you want to stop working, and the income you’ll require throughout retirement. This is where cashflow planning (or as I prefer to call it ‘lifetime income planning’) becomes one of the most valuable tools in financial planning.

Cashflow planning allows you to model your financial future using your current assets, savings, pensions and expected income. Rather than relying on estimates or generic retirement calculators, it creates a personalised forecast to show whether you’re on track to achieve your retirement goals.

Turning Retirement Goals into a Financial Plan

Whilst retirement spending is almost never linear, a cashflow model can help answer important questions such as:

- Where will your retirement income come from?

- How long will your investments and pension savings last?

- When will your State Pension begin?

- Should you draw from pensions, ISAs or other investments first?

- Are there any years where you may face an income shortfall? If so, what can we do between now and retirement to prevent this.

Understanding Your Retirement Income

For many people, retirement income comes from a combination of:

- Workplace and personal pensions

- Annuities and defined benefit / final salary pensions

- ISAs and investment portfolios

- State Pension

- Any other savings or assets

These income sources often begin at different times, and a cashflow forecast can identify any gaps. For example, someone retiring at 57 may need to fund over a decade before becoming eligible for their State Pension. Without careful planning, this could place unnecessary pressure on pension savings or investments.

What If There’s an Assumed Shortfall?

One of several benefits of cashflow planning is identifying potential problems before they happen.

If the analysis shows you may not achieve your desired retirement income, as long as you seek advice early enough, you still have time to make informed decisions. Depending on your circumstances, options may include:

- Increasing pension contributions.

- Investing more into ISAs or other tax-efficient investments.

- Delaying retirement by a few years or working part-time.

- Adjusting your planned retirement spending.

- Reviewing your investment strategy to ensure it remains appropriate for your objectives.

Often, relatively small changes made years before retirement can have a significant impact on your long-term financial security.

Cashflow Planning Scenario

Let’s use Timmy as an example:

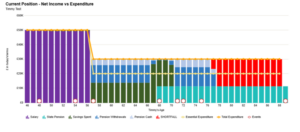

Timmy has just turned 46 and wants to understand when he may be able to retire. Timmy has £150,000 in a stocks and shares ISA and £200,000 in his workplace pension. He would like to retire at age 57 if he can, but he needs £20,000 per year after tax for essential bills and spending and would also like a further £10,000 per year on discretionary spending and holidays.

By bringing together all Timmy’s assets and expected income sources, cashflow planning provides a clear picture of his financial future.

Cashflow planning is based on a range of assumptions, including future investment growth, inflation, income growth and cash savings rates. Based on these assumptions, the analysis has estimated that Timmy would suffer a shortfall in his income needs from age 77.

However, the cashflow plan has also provided Timmy with several solutions to remove this assumed shortfall:

- Delay his retirement to age 62, or

- Reduce his target income by £5,300 per annum, or

- Increase his ISA and pension contributions by £1,000 per month between now and age 57

Planning with Confidence

Rather than attempting to predict the future with certainty, cashflow planning provides a snapshot of your financial position today, allowing you (and Timmy in this instance) to make informed decisions on how to meet your target. Ideally, this should be reviewed regularly as your circumstances, plans and objectives evolve.

At Fiducia, we use cashflow modelling to help clients answer the question: “Do I have enough to retire?”

Whether you’re aiming to retire early or simply want reassurance that you’re on the right track, cashflow planning can provide the clarity and confidence needed to make informed decisions.

Posted in Pensions & Retirement on 14.07.26

{kind=link}