Benefits, Drawbacks And How They Might Benefit You or a Family Member

The Help to Buy ISA scheme became available in the autumn of 2015 and is designed to help first-time buyers gain a foothold on the property ladder. The Lifetime ISA (LISA) was introduced in the budget of March 2016 and will be available from April 2017. The LISA has the dual intention of assisting first-time buyers and helping people to save for retirement.

In this article we provide an overview of each scheme, details of what we believe to be the key advantages and disadvantages of each, together with our view as to how they might benefit you and how they might be used in conjunction with one another. Please note that full legislation for the new LISA is not yet published and therefore details contained herein are based on current information available.

Who can open them?

Help to Buy: first time home- buyers over the age of 16.

LISA: anyone aged 18-39, though you can continue to make subscriptions until aged 50.

What is the closing date for opening a new account?

Help to buy: 30th November 2019, though you can continue to make subscriptions until 1st December 2030.

LISA: currently there is no closing date specified.

What is the bonus?

Help to buy: a bonus of 25% is added to your withdrawal, provided the money is put towards a deposit on your first home (up to the value of £250,000, or £450,000 in London).

The minimum government bonus is £400 (i.e. the value of the account must be at least £1,600 to qualify for a bonus) and the maximum government bonus is £3,000 (i.e. there will be no additional bonus on ISAs valued over £12,000).

Strictly speaking, the bonus is never ‘added’ to the ISA. Instead, your solicitor will apply for it when you purchase your first home.

LISA: each year a bonus of 25% will be added to the total value of subscriptions made in the year. This bonus is added at the end of the tax year.

There is no minimum bonus, however, there is a maximum annual bonus of £1,000 as the maximum annual subscription will be £4,000.

What’s the annual subscription limit?

Help to buy: the ISA can be opened with an initial subscription of up to £1,200. Monthly subscriptions thereafter are capped at £200. Accordingly, subscriptions totalling £3,400 can be made in the first year and £2,400 in all subsequent years.

Note, the monthly subscription allowance works on a rolling basis, that is to say, if you contribute less than £200 in one month, you cannot then contribute the difference in the following month. You effectively lose any monthly allowance you do not use.

LISA: subscriptions totalling £4,000 can be made in the tax year, either as a lump sum, a series of regular subscriptions or a mixture of both.

Withdrawals

Help to buy: money can be withdrawn from the ISA at any time, however, you will only receive the bonus if it is used for a deposit on a house worth up to £250,000 (or £450,000 in London). As with all ISAs, withdrawals do not affect your annual subscription allowance.

LISA: money can be withdrawn from the ISA at any time, however, if the withdrawal is not for one of the following purposes, you will receive no bonus, you will incur a charge of 5% and all interest accrued on the bonus will be reclaimed.

Non-chargeable withdrawals:

- Deposit for a house, worth up to £450,000

- Retirement income (from aged 60)

- Terminal ill health

Provided the monies are used for their intended purpose, each scheme could prove a worthwhile investment. Both ISAs are treated as cash ISAs which means you cannot make subscriptions to another cash ISA in the same tax year as you make subscriptions to either of these accounts. You can, however, still make subscriptions to a stocks and shares ISA.

Like for like comparison: maximum subscriptions for 5 years to buy a house:

| LISA | Help to Buy | |

| Money paid in | £20,000* | £13,000* |

| Bonus | £5,000* | £3,000 |

| £25,000 | £16,000 |

* Note, you will also have received interest (at the rate offered by the account provider).

Provided it is used for either of its intended purposes, the Lifetime ISA is certainly the more attractive of the two accounts: you can invest more, receive a greater bonus and it is more versatile. The 5% charge on withdrawals is certainly a downside, however, the incentive this creates to not draw from the account is, arguably, a good thing. This, in combination with the advent of auto-enrolment legislation, should help people to make better provisions for retirement – an area of financial planning which, historically, many people have either neglected or under-funded.

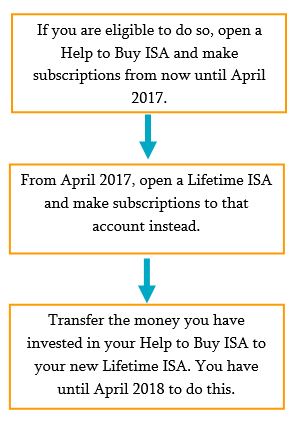

What to do now

The following plan is, in our view, the optimal means of using these ISAs. Please note, however, this may not be appropriate for your personal circumstances and should not be construed as financial advice which should be sought before taking any action or inaction. Please do contact us if you would like to discuss your personal position and requirements.

{kind=link}