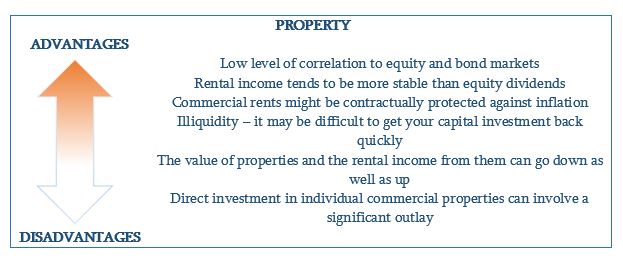

As an asset class, property can polarise opinion. It is often viewed as a relatively illiquid asset in that it can be time-consuming and expensive to trade. Some experts also believe investors are already overexposed to the property sector if they own their own home or a buy-to-let property, or if they are invested in commercial property through their business. However, property can play a part in an income portfolio for those investors who are not overexposed or who are attracted to its potential benefits.

Real estate can indeed be a compelling addition to an income portfolio, particularly when the investment aligns with the investor’s overall strategy and risk tolerance. Properties that are well-maintained or newly renovated, offering no repairs needed, can present a lower risk and more predictable returns. These types of properties often attract higher-quality tenants and can command better rental yields, contributing to a more stable income stream. Additionally, the appeal of such properties can enhance their resale value, providing potential for capital gains.

When it comes to optimizing your real estate investment, selling your property can be a strategic move to either reallocate your assets or capitalize on favorable market conditions. Partnering with professionals who specialize in buying properties can simplify this process. Services that say, We Buy Houses in Long Beach offer a streamlined approach to selling, ensuring a quick and efficient transaction without the hassle of traditional real estate sales. This can be particularly beneficial if you need to free up capital or shift your investment strategy swiftly.

By choosing to sell through these specialized services, you can expedite the process of liquidating your asset and potentially reinvest in properties that better align with your investment goals. Whether you’re looking to diversify your portfolio or take advantage of emerging opportunities, working with experts who offer cash purchases and efficient closings ensures a smooth transition.

RESIDENTIAL PROPERTY

‘Buy-to-let’ is a popular means by which investors gain exposure to residential property. Traditionally, buy-to-let has enabled investors to generate income through rents negotiated on short-term tenancy agreements. More recently, many buy-to-let investors have chosen to use their rental income to finance their own mortgage payments and to wait for the bigger profit in the form of a capital gain when the property is sold. Of course, as some investors have found to their cost, there is no guarantee a property’s market value will rise over the long term.

COMMERCIAL PROPERTY

In contrast, commercial property investment focuses principally on the generation of a high and consistent income that is generated through rents. Whereas residential leases typically operate on a series of short-term agreements, however, commercial leases tend to be much longer – perhaps 10 or 20 years. Income from commercial property can derive from a variety of different sectors – ranging from City real estate, through shopping centres, to industrial parks and warehouses. Each sector commands a different level of rental yield and will react differently to the prevailing economic climate.

COLLECTIVE PROPERTY FUNDS

Direct investment in commercial property is very expensive but smaller private investors can access the asset class through diversified collective funds. Diversification helps to reduce the extent to which the loss of a tenant from one particular property might negatively affect the overall performance of the fund.

REAL ESTATE INVESTMENT TRUSTS

A real estate investment trust or ‘REIT’ is a company that manages a property portfolio on behalf of its shareholders. A REIT can contain residential and commercial property. Its profits are exempt from corporation tax, but it must pay out at least 90% of its taxable income to shareholders.

INVESTING IN PROPERTY SUMMARY

Over the last couple of months we have looked at the options available to investors looking for an alternative to poor cash returns.

KEY FACTORS TO CONSIDER BEFORE INVESTING

Before deciding on the right blend of assets to generate an income stream, you should consider the following factors, which might affect the decisions you make:

INFLATION

The rate of inflation measures how the price of a basket of goods has changed over time. So, for example, if the cost of running your home increases by 5% in a year, you will need to earn 5% a year more to pay for the same level of comfort. If you are aiming to maximise the income from your investments in order to pay for everyday expenses, you should consider the impact of inflation and – particularly over the longer term – whether you require a specific form of protection against inflation. However, if you decide to invest in a fixed-rate investment – for example, a gilt or a corporate bond – be aware inflation will definitely have an impact. As an example, a fixed rate of 4% is attractive when the rate of inflation is 2%. However, if inflation rises to 5%, that return of 4% becomes less appealing.

RISK

Risk is a very personal thing as it can mean different things to different people. Some investors are not prepared to tolerate financial loss in any form while, at the other end of the spectrum, some investors most fear missing out on an opportunity. For still other investors, risk means not being able to meet future financial commitments.

Before formulating an investment strategy, every investor needs to be clear about their investment goals and their tolerance for risk. No investment is risk-free – the lowest-risk investments might guarantee the preservation of capital and/or regular income payments, but they cannot necessarily protect your money against the erosive effects of inflation. Ultimately, in order to enjoy an absence or reduction of risk, a cautious investor has to accept the prospect of lower returns. Equally, an investor who is willing to pursue higher returns will also have to accept the possibility of increased potential for risk to their capital.

DIVERSIFICATION

Since every source of income carries some form of risk, it pays to diversify your portfolio across a range of different asset classes. Diversification helps to reduce the possibility especially weak (or even strong) returns from a particular investment or asset class might have a disproportionate effect on the overall performance of the portfolio.

FIDUCIA’s PORTFOLIO MANAGEMENT SERVICE

We believe that a suitable portfolio can only be designed with a full and detailed understanding of your objectives, risk attitude and tolerance to risk. At the very heart of our investment process is the consideration of how much risk your portfolio should take. As a result all our portfolios have a clearly defined risk budget.

Many firms provide their clients with pre-determined asset allocations that depend heavily upon historical data. While we appreciate the value of such data, we believe that investment portfolios should be forward looking and reflect the economic landscape we live in today, as well as those we are likely to experience in the future. We have developed a strategic asset allocation model which brings together an informed view of the global economy spanning the next decade. This disciplined approach informs our views of asset allocations which are the framework of our investment process.

All of the portfolios are actively monitored on a regular basis and can be viewed online at any time. We provide you with regular reporting, review recommendations, including valuations, performance and market overviews.

Do contact Fiducia so we can show you how sustainable income can be delivered within your own risk profile.