On 11 February 2013, the Secretary of State for Health, Jeremy Hunt MP, announced the Government’s response to the Dilnot Commission report confirming the long awaited reforms which will shape the future of Care Funding in England.

Key Points Of The Care Funding Reforms:

- A cap on lifetime contributions of £75,000 in 2017/18 prices

- An increase in the means tested threshold above which self-funding is required to £123,000 in 2017/18 prices

- A living cost contribution cap of £12,000 per year in 2017/18 prices

- From April 2015 no one will be forced to sell their home to fund care fees, they will instead have the right to defer payment during their lifetime

- National eligibility standards are to be introduced to give greater consistency in access to care.

The lifetime contribution cap and increase to means testing is expected to come into effect from April 2017.

How Will This Affect You?

It should be noted that not all care costs will count towards the contributions cap, only the amount that the Local Authority assess as the benchmark cost of providing the care, in other words the amount that they would otherwise pay. The cost of living expenses such as accommodation and food (known as “hotel costs”) will not count towards the cap. A “living cost” contribution cap of £12,000 per year (£230 per week) has also been proposed and is the amount that all but the poorest will be expected to fund themselves regardless of the lifetime contribution cap.

Although the capital means testing cap will rise from £23,250 to £123,000 in 2017 this does not mean that once assets fall below the £123,000 cap full State funding will be received. There is currently a lower capital means testing limit of £14,250 and this is being retained, although with increases due to inflation it will be around £17,000 in 2017. Any assets between the lower £17,000 limit and the £123,000 cap will be converted into what is known as “tariff income” at a rate of £1 for every £250 of assessable capital and added to other income to calculate an individual’s total contribution to care costs.

The effect of the changes can be illustrated with an example:

Mr A aged 85 has assets of £200,000 (having sold his home) and income of £300 per week including all benefits. He goes into a care home in April 2017 with standard residential care fees of £650 per week. Mr A uses all his income to pay for his care and draws down on capital at a rate of £350 per week to fund the difference. His Local Authority calculates that the maximum they would pay for care for Mr A would be £500 per week. His contribution to the £75,000 cap will therefore only increase by £270 per week (being the £500 Local Authority benchmark cost less the living costs deduction of £230 per week). It would take 5 years for Mr A’s care fees contribution to reach the £75,000 funding cap. During that time he will have depleted capital by over £90,000. At this point Mr A would be eligible for Local Authority funding for his care costs, however, his other income, including tariff income will be taken into account for the so called “hotel” costs as detailed below.

Whilst Mr A’s capital stands at more than £123,000 he would receive no Local Authority funding for care costs in excess of the benchmark less living cost deduction. Once his capital falls below £123,000 the tariff income calculation would come into effect. If we assume that Mr A’s capital has decreased to £110,000 (by age 90 or so given the above scenario) his tariff income would be calculated as:

- £110,000 less the £17,000 lower limit = £93,000 assessable income giving £372 per week tariff income

- When added to his existing income of £300 per week this gives £672 total weekly income.

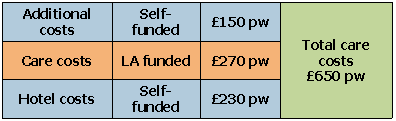

It is understood that once the lifetime contribution cap of £75,000 has been reached, Local Authority funding will be available for the assessed benchmark cost less the living cost deduction. In the case of Mr A this would amount to a Local Authority contribution of £270 per week. Mr A would be expected to continue to self-fund the remaining costs which will be classed as hotel or living costs rather than care costs. In this example, Mr A would therefore need to fund £380 per week or £19,760 per year. It is only at the point his capital reduces below the lower limit of £17,000 that the Local Authority will fully fund his care costs, and then only up to their assessed benchmark cost (£500 in this example).

Simplification?

Whilst prima facie the reforms simplify the current system, the layering of hotel costs and the calculation of the contributions cap against Local Authority costs rather than actual costs is likely to cause confusion.

If we look at a simplified summary of the new system, the layers become more apparent. Taking the above example and assuming the £75,000 contribution cap has been reached, the position would be:

Total self-funded costs £380 per week

Total Local Authority funded costs £270 per week

How Will The Reforms Be Funded?

It is estimated that the reforms will cost £1 billion in 2017. Approximately 80% of this will be funded from increased employer National Insurance Contributions following the proposed introduction of the flat rate State Pension. The remaining 20% will be funded from a freeze in the Inheritance Tax nil rate band at £325,000 until 2019, three years longer than originally proposed.

Shaping The Future

Now the new limits are known individuals can start to plan more effectively for their future. The Government hopes that people will start to save for later life through pensions and other investments. We may see developments in the Long Term Care market, although those in the sector do not believe a resurgence of pre-funded Long Term Care Insurance will occur.

What is important is for everyone to understand the new system and plan effectively for their future. As Tish Hanifan, Joint Chair of the Society of Later Life Advisers commented:

“There is already a huge lack of understanding as to how much care will cost and who will pay for it. This new introduction of slicing out ‘hotel costs’ and setting the ‘financial clock’ for the cap running at Local Authority rates for care funding will make the need for good specialist financial advice even more important if people are to make the best care choices.”

Detailed financial planning incorporating cash flow forecasting will still be essential for many to ensure care fees funding is sustainable. Most home owners will be ineligible for any Local Authority funding for a number of years until the contributions cap is reached and even then those with residual means will be expected to cover at least the “hotel costs” of up to £12,000 per annum. With the average length of stay in care homes being nearer 2 years (source: BUPA) many will never receive any State assistance with their fees.

And whilst the care reforms go some way to tackle the problem of potential catastrophic care costs in the future, it does not help those facing care needs now or in the next four years.

Top Tips

Whilst everyone’s situation will be different, we have detailed below our top tips for Long Term Care funding:

- Ensure a needs assessment is made prior to a financial assessment; where a primary health need exists then NHS Continuing Care should be available (which is fully funded)

- Request a review if health needs change

- Check that all available State benefits, such as Attendance Allowance, are being claimed where appropriate

- Make sure you understand what is included in the cost of quoted care home fees, some care homes assume a deduction for NHS Continuing Care for example

- Seek specialist advice from qualified professionals – lawyers, accountants and financial advisers can work together to create an effective long term strategy to ensure care fees funding remains sustainable whilst accommodating your estate planning wishes.

Fiducia Wealth Management provide specialist Long Tem Care planning advice. Please contact us to discuss how we can help.

© Fiducia Wealth Management Limited 2013